Ten Ways Business Owners Can Lower Their Tax Bills

June 2026

Allen Schaefer, CPA, MBA

Jay A. Friedman, CPA, MST

Bernard M. Holand, CPA, PFS

Operating a business is a demanding and complex endeavor that involves significant responsibilities, particularly in compliance and taxation. For domestic business owners, fortunately, there are several effective strategies available to help minimize the tax burden to preserve more of their hard-earned income. Below are ten practical approaches to reducing tax liability at both the business and individual owner levels:

1. Deduct Business Expenses

According to a Forbes study, a whopping 93% of U.S. business owners may be overpaying their taxes – often because of the extraordinary complexity of the tax code. This presents a risk and an opportunity for a business and its owners. Without a well-structured approach to tax planning to legally minimize tax liability, significant money can be left on the table that could have been reinvested into the business or used for other essential purposes.

The U.S. tax system provides an array of legitimate mechanisms to reduce taxable income, most notably through properly substantiated business expenses. These expenses reduce business net profits and, in turn, overall tax liability. Under Section 162 of the Internal Revenue Code, deductible trade or business expenses must be both "ordinary and necessary"—that is, customary within your industry and appropriate for conducting business. Qualifying categories include wages and compensation, rent, utilities, storage, supplies, taxes and licenses, insurance, repairs and maintenance, dues and subscriptions, travel and vehicle expenses, business meals, and professional services. Additionally, provisions such as Section 179 (see Item 4) allow businesses to immediately deduct the costs of certain capital investments—including equipment, furniture, and software—further enhancing tax efficiency.

2. Utilize the Qualified Business Income (QBI) Deduction

Many business owners can deduct up to 20% of their qualified business income under the QBI deduction, also called the Section 199A deduction. This deduction is available to eligible owners of sole proprietorships, partnerships, S corporations, and LLCs. To optimize your QBI deduction and maximize tax savings, it is important to manage taxable income, optimize wage deductions, time retirement contributions strategically, and aggregate income from eligible businesses. Eligibility rules, income thresholds, phase-out rules, and special limits for Specified Service Trades or Business (SSTBs) can be complex, so consulting a tax professional is wise.

For businesses conducted through a partnership or S corporation, the pass-through deduction is calculated at the partner or shareholder level. Partners and shareholders take into account their allocable shares of each qualified item of income, gain, deduction, and loss from their Schedules K-1. S corporation shareholders only take into account items from their K-1, not any wages the corporation paid them and reported on Form W-2. However, for purposes of the W-2 limitation discussed above, an S corporation's W-2 wages include wages paid to S corporation shareholders, as well as other S corporation officers and employees. The complexities surrounding this substantial deduction can be formidable, and the optimization of shareholder compensation vs distributable K-1 income can have a material impact on the allowable deduction, which can produce a tax benefit exceeding additional payroll taxes associated with additional shareholder compensation.

3. Utilize State Pass-Through Entity Tax (PTET) Elections

As mentioned in our previous PW Tax Alert, for Tiered Partnerships and Investment Partnerships, within the tax community, there are differences of opinion on where geographically the federal deduction for PTE taxes gets reported on the PTE's tax returns and Schedule K-1s. When considering making a PTE election, know that this is a complicated tax strategy that requires consulting with a tax professional.

4. Invest in Equipment and Technology

The One Big Beautiful Bill Act (OBBBA) permanently reinstated the 100% bonus depreciation deduction, under Section 168(k), for qualified property acquired and placed in service after January 19, 2025. However, taxpayers can elect out of bonus depreciation only for an entire "class" of property. This election-out may defer more depreciation than the taxpayer wants to. But because Section 179 elections are made on an asset-by-asset basis, to achieve a desired amount of current-year depreciation, a taxpayer may elect to treat Section 179 property as an expense for only some of the assets for which the election out of bonus depreciation was made. Example of a business with a $3,000,000 qualified equipment purchase in 2026:

Section 179 Deduction: $2,560,000 (Maximum allowed in 2026)

Bonus Depreciation Deduction: $440,000

Total Tax Savings: $1,110,000 (assumes a 37% federal individual tax rate. Note: Additional state tax savings may apply)

Net Initial Year Final Equipment Cost: $1,890,000

At the State level, some states conformed to OBBBA while others, to protect state revenues, explicitly rejected OBBBA's federal tax changes and required add-back modifications. This variation creates a complex compliance environment, requiring careful state-by-state analysis for tax planning and reporting purposes. Before making a large purchase, it can be helpful to review how different depreciation options may affect cash flow and taxes, including state tax implications due to differing state treatment of depreciation vs Section 179 expense.

5. Time Income and Expenses Strategically, Paying Employee Bonuses

Many people wait until the end of the year to start thinking about their taxes, but by then, it may be too late to make any significant changes. Instead, one should plan throughout the year. Accelerating expenses and deferring income near year-end can lower taxable income for the current year. This shifts taxable income to a future year, which may be in a lower tax bracket or with more deductions. Conversely, in an anticipated lower tax bracket year, the opposite should be done, where income acceleration yields a greater tax benefit. This requires careful planning to avoid cash flow issues.

Paying Employee Bonuses: For Cash-Basis Businesses, you must pay the bonus before the end of your tax year, usually December 31st, to deduct it in that year. However, for Accrual-Basis Businesses, you can deduct a bonus accrued in one year if it is paid out within 2.5 months of the year-end (i.e., by March 15th for a calendar year business), and the liability was fixed and determinable by the year-end. Owner-Employee Alert: The 2.5-month rule doesn't apply to related parties, such as an owner of an S Corporation who is also an employee or a family member. For related parties, you can only deduct the bonus in the year it's actually paid.

6. Employ Family Members

Hiring your spouse or children for legitimate business work can shift income into their lower personal tax bracket, creating additional business deductions, and potentially reducing overall family tax liability. Wages paid to family members are deductible as ordinary business expenses provided that the work is legitimate and properly documented, the pay is reasonable, and you follow labor laws. Children under 18 are not subject to FICA (Social Security/Medicare) taxes, and are not subject to FUTA (Unemployment) taxes until age 21. For 2026, the standard deduction is $16,100, so a child can earn up to that amount tax-free.

From their earned income, family members can make Traditional IRA (pre-tax) or Roth IRA (post-tax) retirement contributions, up to limits set by the IRS, provided they meet eligibility requirements. The contribution limits for 2026 are $7,500 for individuals and $8,600 for those aged 50 or older. To achieve significant tax-free income that is without any Required Minimum Distributions (RMDs), family members should consider a Roth IRA. Unlike Traditional IRAs, which are retirement account that allows individuals to make pre-tax contributions and are taxed upon receiving RMDs later in life, the IRS does not require the original account holder of a Roth IRA to ever take any RMDs.

Where a family member's income exceeds certain IRS income thresholds, utilize the Backdoor Roth IRA strategy - see this PW Tax Alert for more info.

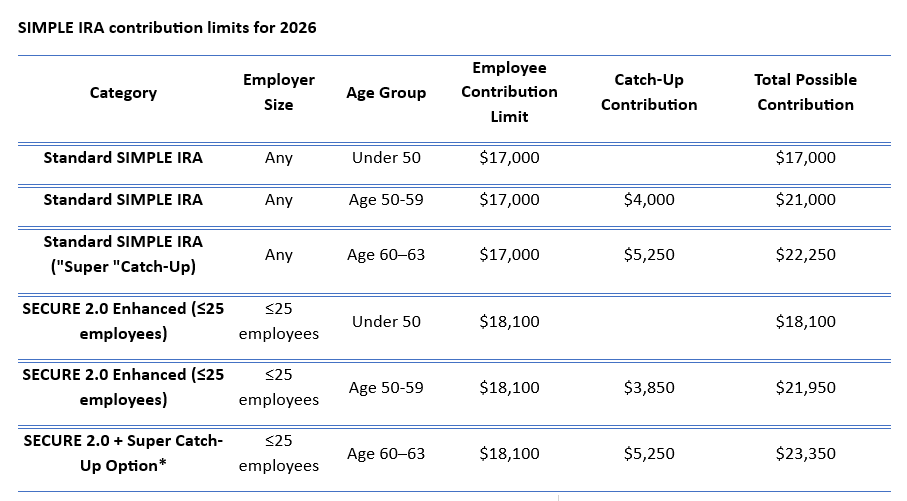

7. Consider Retirement Contributions

For business owners, contributions to a Retirement plan such as a SEP IRA, Solo 401(k) (for self-employed only), SIMPLE IRA or defined benefit plan (i.e., Cash Balance) not only secure your future but also come with tax benefits. By putting more of your income into these accounts (within limits), you lower your current tax bill, which can be especially valuable if you're in a higher tax bracket. Contributions are generally made with pre-tax dollars and can grow tax-deferred until you withdraw the funds in retirement. At the time of withdrawal, you pay ordinary income taxes on the pre-tax contributions and growth. Alternatively, a Roth IRA, which is funded with after-tax dollars, offers tax-free growth and withdrawals. Where one's income exceeds certain IRS income thresholds, utilize the Backdoor Roth IRA strategy - see this PW Tax Alert for more info.

Other retirement plans, not shown above, such as SEP IRA, Solo 401(k) plans, or defined benefit plans (i.e., Cash Balance) allow for even greater deferrals and are not taxed until distribution.

8. Take Advantage of Home Office Deductions

If you're self-employed, running a small business, or freelancing, you could save money on your taxes by claiming home office expense deductions. If you use part of your home exclusively for business, you can deduct a portion of your rent, mortgage interest, utilities, and insurance. Per the IRS, the home office deduction can be calculated in one of two ways:

Actual expense method. Calculate the percentage of your home used for business and apply it to the total expenses for that portion of the home. If you worked from home for only part of the year, adjust your calculation accordingly.

Simplified method. Deduct $5 per square foot of your home office, up to 300 square feet. For example, if your office is 300 square feet and you worked from home for nine months, your deduction would be $1,125 (300 * $5 * 9/12).

9. Claim Health Insurance Deductions

Self-employed business owners may be able to deduct 100% of health insurance premiums for themselves, their spouse, and dependents, including medical, dental, and qualifying long-term care coverage, even if they do not itemize deductions. For many families, this can represent a substantial tax benefit.

However, this deduction is generally not available if the taxpayer is eligible to participate in a subsidized employer-sponsored health insurance plan, including coverage available through a spouse's employer. A subsidized plan is one in which the employer pays a portion of the insurance premium.

10. Tax Planning for Multi-State Businesses

Businesses operating across multiple states should carefully evaluate the impact of state and local income and franchise taxes. A key consideration is selecting a tax-efficient entity structure that accounts for nexus, as establishing a presence in a state can trigger additional tax liabilities and filing requirements. Analyze state tax rates and income sourcing methodologies—such as cost of performance versus market-based sourcing—to achieve more favorable apportionment outcomes. In addition, understanding state conformity rules is critical, since some states decouple from federal provisions, including bonus depreciation, R&D expensing, interest expense limitations, and the treatment of net operating losses. Further, businesses should explore available state tax credits and incentives (i.e., job creation, R&D, investments in distressed areas, investing in renewable energy) and work with economic development agencies to maximize their benefits.

Work with a Tax Professional Year-Round

Taxes can be complex, and regular proactive tax planning to navigate evolving tax laws —not just annual tax return preparation—can make a substantial difference to your bottom line. Working with a tax professional year-round to develop tailored strategies to support your long-term goals can help you avoid costly mistakes.

At Perelson Weiner, we understand the unique challenges facing businesses and work closely with our clients to identify tax-savings opportunities, deductions, and credits that might otherwise be overlooked, helping business owners retain more of their hard-earned profits in a thoughtful and tax-compliant manner. For additional information, please contact your Perelson Weiner professional.